Tool -

Tool -

D2.04

Tool -

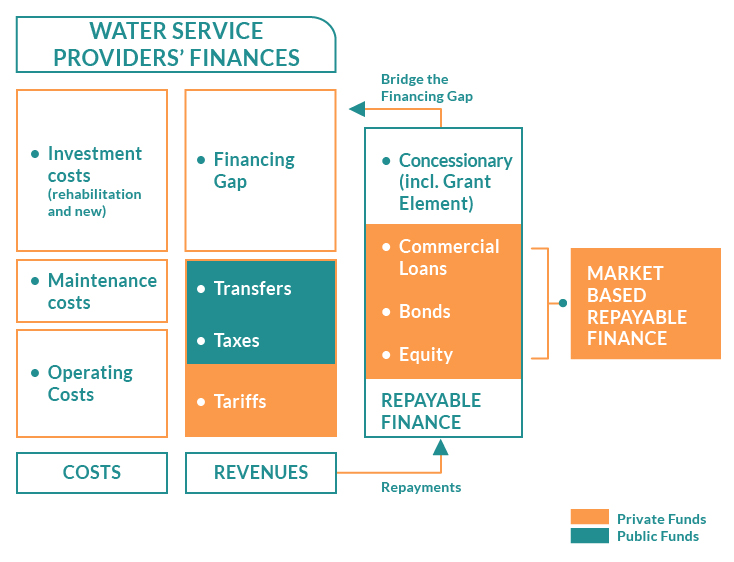

Private or public water and sanitation service providers need financial resources to make infrastructure investments with high upfront costs and to operate and maintain them. This means utilities need to leverage investment capital and working capital through loans, bonds, and/or equity, known as repayable finance mechanisms (Figure 1). The main source of capital are development banks (national or international), financial institutions (such as commercial banks), and institutional investors (sovereign wealth funds, insurers, pension funds, private equity funds, endowment funds, among others). International development banks, such as World Bank, Interamerican Development Bank, African Development Bank, Asian Development Bank, and European Bank for Reconstruction and Development played a key role in promoting private participation in water provision.

Figure 1. How Repayable Finance Works (Adapted from OECD, 2010).

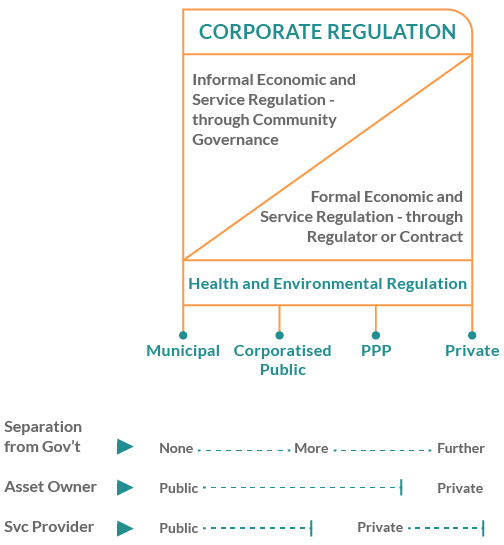

Water service providers can be either public or private companies depending on institutional arrangement society has agreed on and the values it has decided to pursue to achieve a desired social outcome. Rouse (2013) identifies four business models: municipal, corporatised public, private-public partnerships (PPP), and private. They differ in terms of “the degree of separation from government, asset ownership, and whether the [provider] is public or private” (Rouse, 2013; see Figure 2). This classification is not broad enough to include community-based organisations, that is, when communities organise to provide water themselves without the intervention of government (Bakker, 2010). Under Rouse’s parameters of classification, the latter are fully private, however, ownership is collective.

Figure 2. Main Business Models for Water Service Providers (Adapted from Rouse, 2013).

Each of these business models has specific features that make them more or less attractive for investors. For example, the public and corporatised models are more suitable for indirect investments such as loans or bonds. Governments may take credits directly from development banks or commercial banks on behalf of the public agency in charge of supplying WASH. Corporatised public utilities may also issue bonds and back them with a “sovereign guarantee” (a financial clause by which the national government assumes the service of debt in the case of default). On the other hand, PPPs and private utilities are more interesting for private financiers. The former is a hybrid in which assets ownership is retained by the state (local, regional, or national governments) while management is transferred to a private provider that has as a main driver is to profit from operating water infrastructure (Marin, 2015). Both PPP and private utilities may also be recipients of loans and bonds and, in some cases, they might also issue equity through a public offering, in the local stock exchange, or privately, for specific investors.

A key aspect to attract financing sources for any of these types of service provider is “creditworthiness”. This is a measure of a borrower’s ability and willingness to service its debt obligations. To be creditworthy, a utility must demonstrate a reliable stream of positive cash flow from operations as well as sufficient cash reserves in the case that future cash flows are not sufficient. The degree of creditworthiness is judged through a valuation performed by lenders or independent parties to determine the borrower’s potential for defaulting on its debt obligations. There are various tools available for assessing credit, from creditworthiness indexing to shadow ratings to credit ratings (World Bank, 2017).

Aside from the 3Ts (tariffs, taxes, and transfers (Tool D2.03), water service providers can also tap into loan, bond and equities to finance their activities (Table 1). The categorization of the financing instrument depends based on a variety of features including: (i) interest rates (the price paid from borrowing money), (ii) the repayment period or date (tenor), (iii) whether there is a grace period before repayment starts, (iv) the security (collateral) required, and (v) its conditionality (actions to be undertaken by the borrower as a condition for getting the funding) (WWC & OECD, 2015).

Table 1. Categories and Sources for Water Investments. Source: WWC-OECD (2015).

| 3Ts & Other contributions to recurrent finance | Loan & bond finance | Equity finance |

|---|---|---|

| Tariffs & user charges | Public development banks | Institutional investors |

| Taxes (national budgets) | Commercial banks (inc. project finance) | Sovereign Wealth Funds |

| ODA | Institutional investors | Specialised water funds |

| Philanthropic funds | Sovereign Wealth funds | International Financial Institutions |

| Property taxes & other levies & contributions | Public bond issue | Private equity funds |

| Self finance by users | International Financial Institutions | Venture capital |

| Project Bonds | Public-Private partnerships | |

| Microfinance | Individual shareholders | |

| Climate finance | ||

| Export credits | ||

| Individual bondholders |

A loan takes the legal form of a traditional lending product where a private or public borrower obtains credit from a bank in return of a financial commitment (interest rate) to use the proceeds to finance projects or assets. Loans exist in various kinds:

Bonds are debt instruments issued by either public or private organisations to raise capital in the domestic and international capital markets (public offering) or placed privately with a limited number of investors (not listed on a public exchange). Bonds issued by municipalities and other sub-sovereign bodies often depend on credit enhancement of various kinds (guarantees). Investors receive full repayment of the bond issuance amount (the principal) in addition to interest payments on outstanding principal amounts (the coupon payments) (Deutz et al., 2020). Some of the most important types of bonds used in the water sector are:

Finally, equity is a financing instrument through which utilities raise capital through public equity markets by selling shares to investors through organised stock exchanges. Shares are considered to be perpetuities and confer ownership rights to shareholders (prospective capital gains and dividends) and might be a form of long-term investment finance for water infrastructure (OECD, 2015). Equity capital can be provided both by private and public partners. Although equity is the most flexible form of capital, in the long term it needs to earn rates of return conforming to market expectations. The following are examples of the use of equity to finance water projects:

Private investors also use different vehicles to access equity in water utilities such as specialised water funds (dedicated to acquiring securities pertaining to water), private equity funds (typically buying ownership through equity in companies with good prospects of profit) or venture capital (equity invested in startup or small on-going companies related to untested water technologies), and Public-Private Partnerships (if the company that gets the contract is organised as a Special Purpose Vehicle).), Special Purpose Vehicles (i.e., a subsidiary company that is created as a separate legal entity which is intended for a specific purpose) have yet to become a popular financing instrument for the water sector, although there is now a few good examples emerging (e.g., OECD, 2019).

Water sector actors and projects need to manage different types of risks:

All those risks can affect the profitability of a water business and thus can be ultimately translated as a financial risk for lenders, investors, sponsors, bond holders and all others exposed to water projects, business models, service providers etc. These are the risks of them losing their money through their involvement in water infrastructure and services. The leverage of a given flow of basic revenues (“3Ts”) for attracting repayable finance can be enhanced by using various kinds of risk-sharing and risk-mitigation instruments. Guarantees work either by mitigating specific risks that would otherwise hamper financing, or by packaging the finance in a form that is more attractive to potential financiers. For credit enhancement, which describes any form of public intervention to increase the likelihood of debt repayment, the most common financial guarantees are (a complete taxonomy of guarantees for mitigating risks in infrastructure projects is provided in Table 2):

Table 2: Financial Risk Mitigants and Incentives for Infrastructure Finance. Source: OECD (2015).

Here are some key lessons in terms of finding sustainable financing solutions for water projects: